Active vs Passive Investing: What Investors Should Understand Before Choosing a Strategy

When building an investment portfolio, one of the most common questions is whether to use active investment funds, passive investment funds, or a combination of both.

It is an important question, but it is often presented too simply.

Active investing is not automatically better because a fund manager is making decisions. Passive investing is not automatically better because it is usually lower cost. The right approach depends on what the investor is trying to achieve, the level of risk being taken, the overall structure of the portfolio, the costs involved and how the investments fit into a wider financial plan.

For many clients, the real issue is not whether active or passive investing “wins”. It is whether the investment strategy is suitable, properly diversified, cost-conscious and aligned with their long-term goals.

Image title: Active vs Passive Investing EWS Financial Advisers

Alt text: Chartered financial planner reviewing active and passive investment options for a client portfolio

What is active investing?

Active investing involves a fund manager or investment team making decisions about which assets to buy, hold or sell. The aim is usually to outperform a particular market, benchmark or peer group.

An active fund manager may look for companies they believe are undervalued, avoid sectors they consider unattractive, adjust the portfolio in response to changing market conditions, or use research to identify opportunities that are not fully reflected in market prices.

The appeal of active investing is clear. In theory, a skilled manager may be able to add value by making better decisions than the wider market. This can be particularly attractive in areas where markets are less efficient, specialist knowledge matters, or where risk management is especially important.

However, active management also introduces additional considerations.

Active funds usually have higher charges than passive funds. The manager has to outperform not only the market, but also the additional cost of running the fund. There is also no guarantee that an active fund manager will outperform. Some active managers do add value over certain periods, but others underperform the market after costs. Even strong managers can go through long periods where their style is out of favour.

This means active investing should not be chosen simply because it sounds more sophisticated. It should be considered carefully, with attention paid to the manager’s process, track record, charges, risk controls and role within the wider portfolio.

What is passive investing?

Passive investing aims to track the performance of a market index or benchmark, rather than trying to beat it.

A passive fund might track an index such as the FTSE All-Share, S&P 500, MSCI World or another defined market. The fund is designed to follow the market as closely as possible, usually at a lower cost than active management.

The main appeal of passive investing is simplicity, transparency and cost efficiency. Instead of relying on a fund manager to pick winners, the investor gains broad exposure to a market or asset class.

Passive investing can be particularly useful where markets are highly competitive and well researched. In these areas, consistently outperforming after charges can be difficult. Lower costs can therefore make a meaningful difference over the long term.

However, passive investing is not risk-free.

A passive fund will generally rise and fall with the market it tracks. If the index falls sharply, the fund is likely to fall too. Passive investing also means accepting the composition of the index. If a particular sector, region or group of companies dominates the index, the investor will usually be exposed to that concentration.

Passive investing can be a useful tool, but it still needs to sit within a properly constructed investment advice strategy.

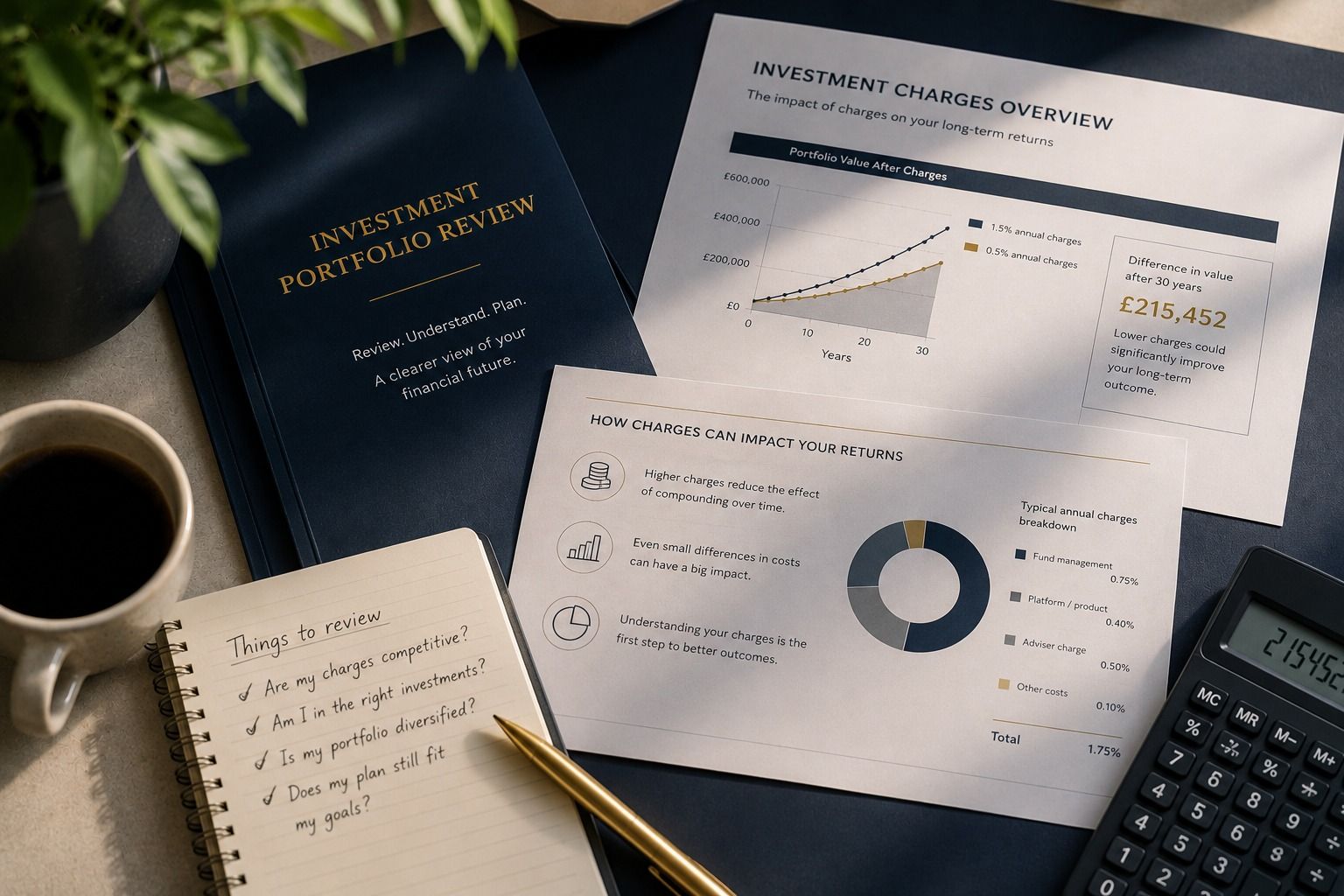

Cost matters, but it is not the only factor

Cost is one of the strongest arguments in favour of passive investing.

Lower charges mean more of the investment return stays with the investor. Over long periods, even small differences in annual charges can compound into meaningful differences in outcome.

That said, cost should not be considered in isolation.

A low-cost fund is not automatically suitable. It may expose the investor to the wrong level of risk, the wrong asset class, the wrong geography, or a concentration they do not fully understand.

Equally, a higher-cost active fund is not automatically unsuitable. If it plays a clear role in the portfolio, offers genuine expertise, manages risk effectively or provides exposure that is difficult to access passively, it may be appropriate.

The important question is not simply: “Which fund is cheapest?” It is: “Is the total investment strategy suitable, diversified, cost-effective and aligned with the client’s goals?”

Active and passive investing can work together

The active versus passive debate is often presented as if investors must choose one side.

In practice, many well-constructed portfolios use a blend of both.

Passive funds may be used for broad market exposure where low-cost access is appropriate. Active funds may be used selectively in areas where specialist management may add value, where markets are less efficient, or where a particular investment approach is required.

For example, a portfolio might use passive funds for developed market equity exposure, while using active managers in areas such as smaller companies, specialist bonds, commercial property, infrastructure, absolute return strategies or other areas where manager skill may be more relevant.

The key is not whether a portfolio is active or passive. The key is whether every part of the portfolio has a clear purpose.

Suggested image: adviser reviewing portfolio allocation, fund charges and risk spread across pensions and investments.

Suggested alt text: Financial adviser reviewing investment portfolio diversification and charges with a client

The role of diversification

Diversification is one of the most important principles in investment planning.

A portfolio should not depend too heavily on one fund, one manager, one market, one sector or one investment style.

Active funds can introduce manager-specific risk. Passive funds can introduce index concentration risk. Both need to be understood.

A properly diversified portfolio will usually consider:

- Asset classes

- Geographic exposure

- Sector exposure

- Investment style

- Currency exposure

- Risk level

- Liquidity

- Charges

- Tax position

- Time horizon

The aim is not to remove risk entirely. That is not possible. The aim is to take appropriate risk in a structured and considered way.

Investment choice should start with the financial plan

One of the biggest mistakes investors make is starting with the fund choice.

They ask whether they should use active funds or passive funds before answering the more important questions.

Before choosing investments, it is worth asking:

- What is the money for?

- When might it be needed?

- How much risk is appropriate?

- What level of loss could be tolerated?

- Is income required?

- Is the investment linked to retirement planning?

- Are there tax considerations?

- How does this fit with pensions, ISAs, savings, property or business wealth?

- What would a successful outcome look like?

Only once those questions are clear should the investment structure be built.

For some clients, the priority may be long-term growth. For others, it may be retirement income, capital preservation, inheritance planning, tax efficiency or maintaining flexibility. This is where investment planning often needs to connect properly with wider pension and retirement planning, rather than being treated as a separate decision.

The investment strategy should follow the plan, not the other way around.

Reviewing an existing portfolio

Many investors already hold a mixture of funds collected over time.

They may have old pensions, ISAs, general investment accounts, workplace schemes or inherited investments. Over the years, these can become fragmented, expensive or poorly aligned with the client’s current needs.

A portfolio review can help answer questions such as:

- Are the investments still suitable?

- Are the charges reasonable?

- Is there unnecessary duplication?

- Is the risk level appropriate?

- Is the portfolio too concentrated?

- Are active funds adding value?

- Could passive funds reduce costs in certain areas?

- Are the investments tax-efficient?

- Does the portfolio still match the client’s objectives?

This is particularly important when approaching retirement, changing career, selling a business, inheriting money, planning for income, or reviewing long-term family wealth. Clients who want local support may also benefit from speaking to a financial adviser in Edinburgh who can look at the full picture, not just the fund list.

Active vs passive investing: the EWS view

At Executive Wealth Services, we do not believe the active versus passive debate should be treated as a slogan.

The question is not whether active investing is always better or passive investing is always cheaper.

The question is whether the investment approach is suitable for the individual client.

That means looking at the client’s objectives, risk profile, tax position, time horizon, existing holdings, pension arrangements, income needs and wider financial plan.

For some clients, passive investments may provide efficient, low-cost market exposure. For others, selected active management may have a role. For many, a carefully blended approach may be appropriate.

The important point is that the investment strategy should be intentional.

Every fund, wrapper and investment decision should have a reason for being there.

When should you review your investment approach?

It may be worth reviewing your investment strategy if:

- You are unsure what you are invested in

- You have pensions or investments in different places

- You are approaching retirement

- Your circumstances have changed

- You are concerned about charges

- Your portfolio has not been reviewed for several years

- You are taking more risk than you realised

- You are not sure whether your investments are still suitable

- You want a clearer long-term financial plan

A review does not always mean making major changes. Sometimes it confirms that the existing approach remains suitable. In other cases, it highlights areas where costs, risk, diversification or structure could be improved.

Speak to EWS about investment advice

Executive Wealth Services provides independent financial planning and investment advice in Edinburgh, Glasgow and across Scotland.

If you would like to review your investments, understand your pension arrangements or consider whether your current portfolio remains suitable, EWS can help you look at the full picture.

Review your investment approach with EWS

If your pensions, ISAs or investment accounts have not been reviewed for some time, a structured conversation can help clarify whether your current approach still fits your goals, risk profile and wider financial plan.

The value of investments can fall as well as rise, and you may get back less than you invested. This article is for general information only and should not be treated as personal financial advice.

Recent Posts