From April 2027, unused pensions may form part of your estate for inheritance tax. Learn what the change could mean for retirement and estate planning.

Meta description:

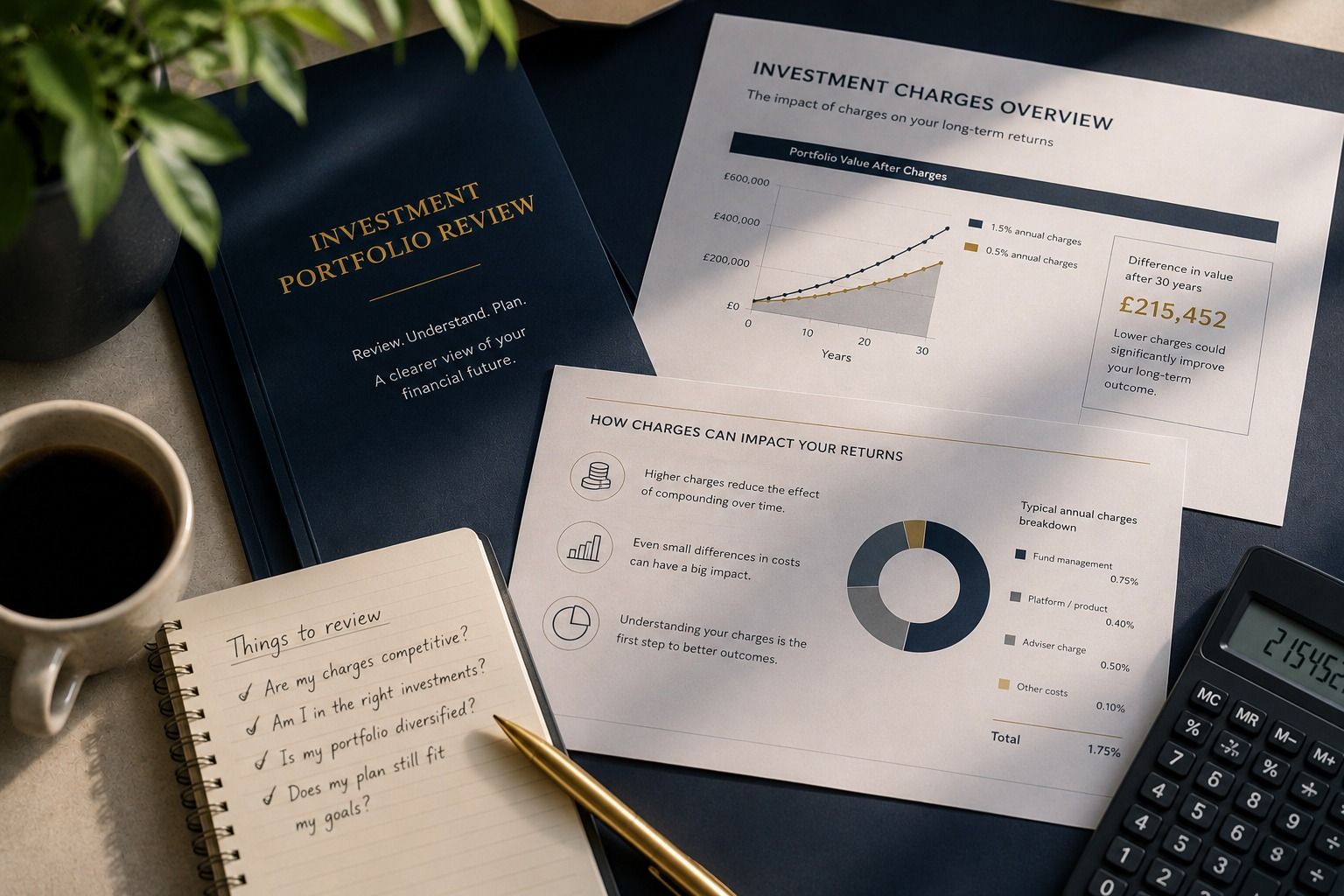

Review pension and investment charges with EWS. Understand fund costs, platform fees, adviser charges and long-term portfolio value.

Review pension and investment charges with EWS. Understand fund costs, platform fees, adviser charges and long-term portfolio value.

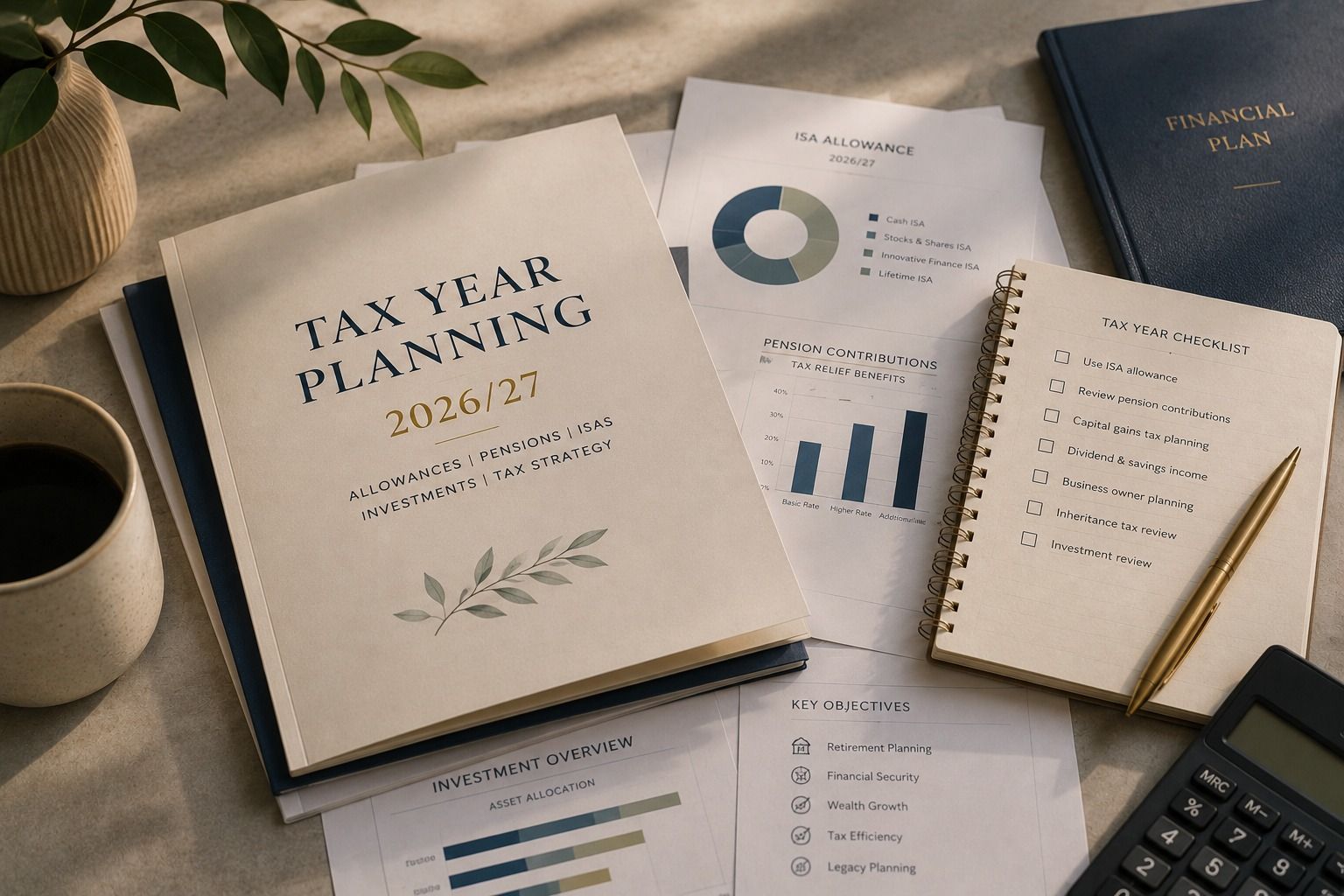

Tax year planning for 2026/27. ISAs, pensions, CGT allowances and investment planning from EWS Financial Advisers in Edinburgh and Glasgow.

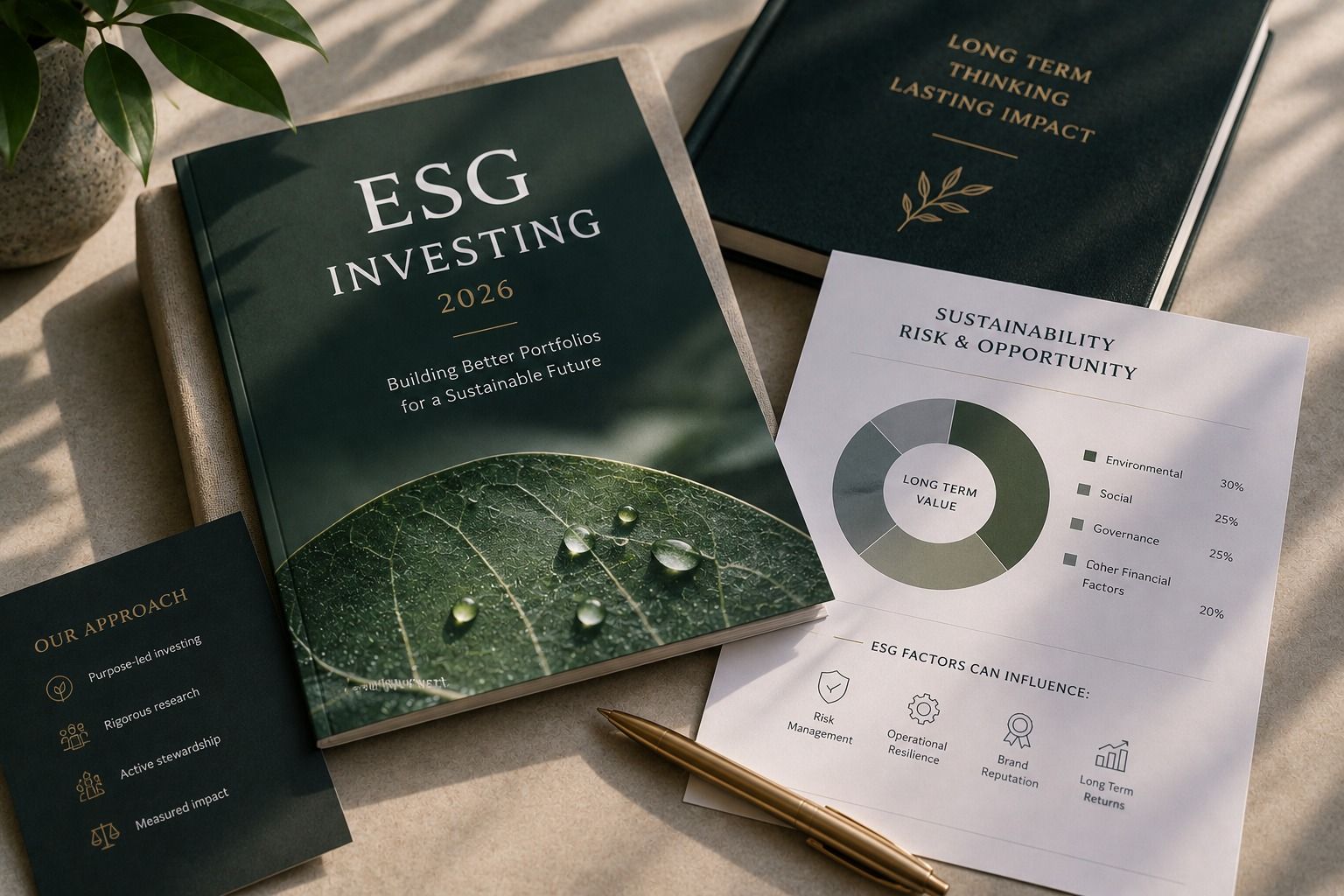

Understand active vs passive investing, costs, diversification and long-term portfolio planning from EWS Financial Advisers in Edinburgh and Glasgow.